For most Indian families, a home is more than just four walls and a roof; it represents a lifetime of hard work, emotional investment, and financial security. We spend decades planning for that perfect 2BHK or 3BHK, often taking on significant debt to make the dream a reality. However, there is a harsh regulatory framework that every homeowner must understandthe SARFAESI Act.

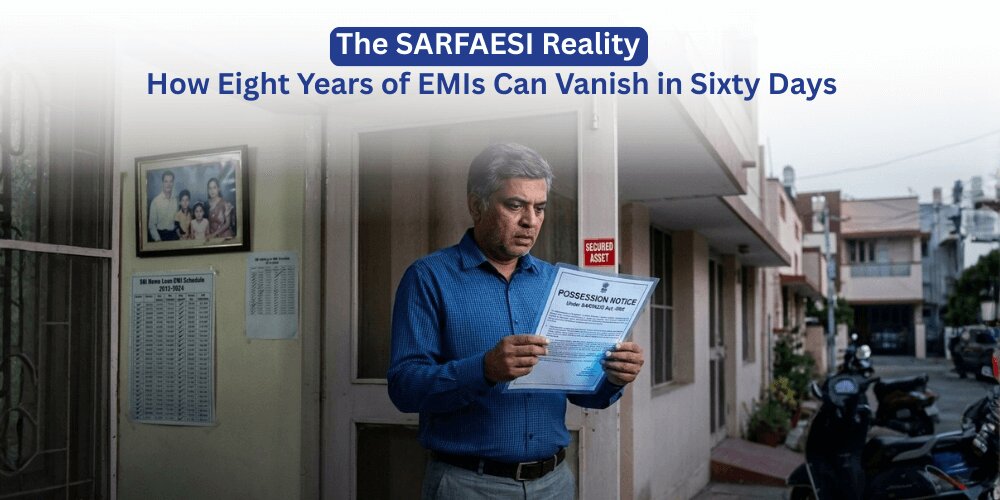

A recent, harrowing case in the Indian real estate market serves as a wake-up call for every borrower. Imagine a family that diligently paid their home loan instalments for eight long years. They built equity, improved the property, and treated the house as their ultimate safety net. Yet, after missing just three consecutive instalments due to unforeseen financial distress, the bank initiated a process that saw them lose a property worth ₹1.2 crore in a mere sixty days.

This isn’t just a cautionary tale; it is the legal reality of debt recovery in India. At Legal Assure, we believe that informed borrowers are protected borrowers. Here is a deep dive into how the SARFAESI Act works and what you can do to shield your assets.

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) was enacted to give banks and financial institutions a faster route to recover bad loans. Before this law, banks had to navigate the sluggish corridors of civil courts to seize assets from defaulters, a process that could take decades.

Under SARFAESI, the requirement for court intervention is largely removed for "secured assets"properties you pledge as collateral for a loan. If you stop paying, the bank has the power to take over your property, auction it off, and recover its dues without needing a judge’s permission. While this has improved the health of the banking sector, it has left many honest but struggling borrowers vulnerable to aggressive recovery tactics.

The transition from being a "proud homeowner" to a "defaulter" happens much faster than most people realise. The timeline is unforgiving:

This is exactly what happened in the ₹1.2 crore home loan case. Despite eight years of successful payments, the law does not look at your past track record once the 60-day notice expires. The bank's primary objective shifts from "customer service" to "asset liquidation."

A common misconception among borrowers is that their "intent" or "history" will protect them. You might think, "I have paid 70% of the loan; surely the bank will understand a temporary job loss?"

Unfortunately, the SARFAESI Act is a mechanical law. It doesn't account for your child’s school fees or a medical emergency in the family. Once the clock starts ticking on a Section 13(2) notice, the bank is on a legal rail-track. In the reference case we analysed, the rapid escalation meant that the equity the family had built over nearly a decade was wiped out. When a property is auctioned by a bank, it is often sold at a "distress value," which is significantly lower than the actual market price. The borrower loses the home, the appreciation of the property, and the peace of mind they worked so hard to build.

While the SARFAESI Act is powerful, it is not absolute. Borrowers have specific legal rights that can be used to stop or delay the process, provided they act quickly:

Prevention is always better than a legal battle in the DRT. If you feel your financial situation is slipping, do not wait for the notice.

The dream of homeownership shouldn't turn into a legal nightmare. The SARFAESI Act is a reminder that the fine print in your loan document carries immense weight. Losing a ₹1.2 crore asset after eight years of discipline is a tragedy that is often preventable with the right legal intervention at the right time.

At Legal Assure, we specialise in helping borrowers navigate these complex financial waters. Whether it is responding to bank notices or representing your interests in the Debt Recovery Tribunal, our goal is to ensure that your home remains yours. Don't let sixty days erase years of hard work. Be proactive, stay informed, and protect your legacy.

What exactly is a Section 13(2) notice under the SARFAESI Act?

It is a formal demand notice issued by a bank once a loan account is classified as an NPA, giving the borrower exactly 60 days to discharge their full liability. Failure to comply or raise a valid legal objection within this window allows the bank to take physical possession of your property without a court order.

Can a bank sell my house if I have already paid more than 70% of the loan?

Yes, the SARFAESI Act does not consider the percentage of the loan repaid; it only focuses on the current default and the "secured asset" status. Even if only a small fraction of the debt remains, the bank holds the legal right to auction the entire property to recover the outstanding balance and associated costs.

What is the best way to stop a bank auction once a notice is received?

The most effective strategy is to immediately file an application before the Debt Recovery Tribunal (DRT) to challenge the procedural validity of the bank’s notice. Simultaneously, engaging in a "One Time Settlement" (OTS) or requesting a loan restructure can provide a non-litigious path to saving your property from the hammer.

How many missed EMIs will trigger the SARFAESI recovery process?

Typically, if you miss three consecutive monthly instalments, the bank will classify your account as a Non-Performing Asset (NPA) after the 90-day mark. Once the NPA status is locked in, the bank is legally empowered to initiate the recovery process, starting with the 60-day demand notice.

Does the bank have to return the extra money if my house sells for more than the debt?

Legally, yes; the bank is only entitled to recover the principal, interest, and any legal or auction-related expenses they incurred. Any surplus funds remaining from the auction proceeds after satisfying the bank's total dues must be returned to the borrower, though this process often requires careful auditing.